Investment planning for retirement should support the retirement paycheck your broader plan is designed to provide.

This article may be especially helpful if you are within five years of retirement, recently retired, or wondering whether your portfolio is still structured appropriately after recent market volatility.

If you have spent decades saving carefully, it is natural to feel more protective of your portfolio as retirement approaches.

Market uncertainty can feel especially personal when retirement is near or already underway. During the working years, market declines may be uncomfortable but easier to endure because there is usually time, employment income, and continued savings on your side. In retirement, the same decline can raise a more immediate question: Will my portfolio still support the life I hope to live?

That concern is understandable. Retirement investment planning is not simply about choosing funds or trying to predict the market. It is about designing a portfolio that supports the income plan, provides liquidity for planned withdrawals, helps manage risk, and remains aligned with the broader retirement plan through both calm and difficult markets.

At Kastler Financial Planning, our investment philosophy is planning-first. Through 7 Pillars Investment Planning® and, where appropriate, 7 Pillars Purpose-Driven Portfolios™, we evaluate investment decisions in relationship to retirement income planning, dependable income sources, tax considerations, risk capacity, time horizon, personal goals, and values. The goal is not speculation. The goal is thoughtful portfolio design that helps support a coordinated retirement paycheck with greater clarity and discipline.

This article offers historical perspective on market volatility, then explains how retirement investment planning can be coordinated with retirement income planning, including the retirement paycheck, income floor, portfolio structure, bucket strategy, risk management, and ongoing review.

Historical Market Perspectives

History cannot remove uncertainty, but it can provide context. Markets have experienced corrections, bear markets, recessions, inflationary periods, financial crises, and sudden shocks. In many cases, disciplined investors who remained invested through difficult periods participated in later recoveries. That does not mean every decline feels easy or that future recoveries are guaranteed. It does mean that retirement planning should be built with market uncertainty in mind rather than surprised by it.

The visuals that accompany this article illustrate three important ideas: the challenge of timing the market, the frequency and recovery pattern of market corrections, and the reality of bear markets. Each point matters, especially for retirees who may be taking withdrawals while markets are unsettled.

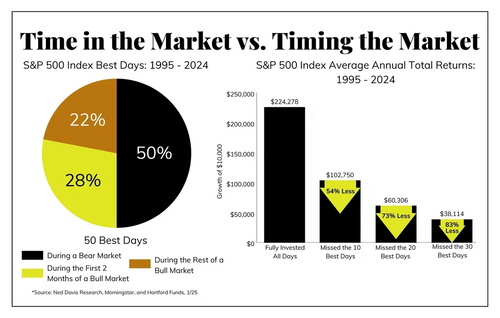

Time in the Market vs Timing the Market

Trying to move in and out of the market can create two difficult decisions: when to sell and when to reinvest. Missing only a small number of strong market days may have a meaningful effect on long-term results, and some of the strongest days have historically occurred during or near difficult market periods.1

For retirees, this does not mean blindly ignoring risk. It means the portfolio should be designed in advance around the income plan it is meant to support. When near-term spending needs, dependable income sources, and longer-term growth assets are considered together, short-term market fear is less likely to become the primary driver of long-term investment decisions.

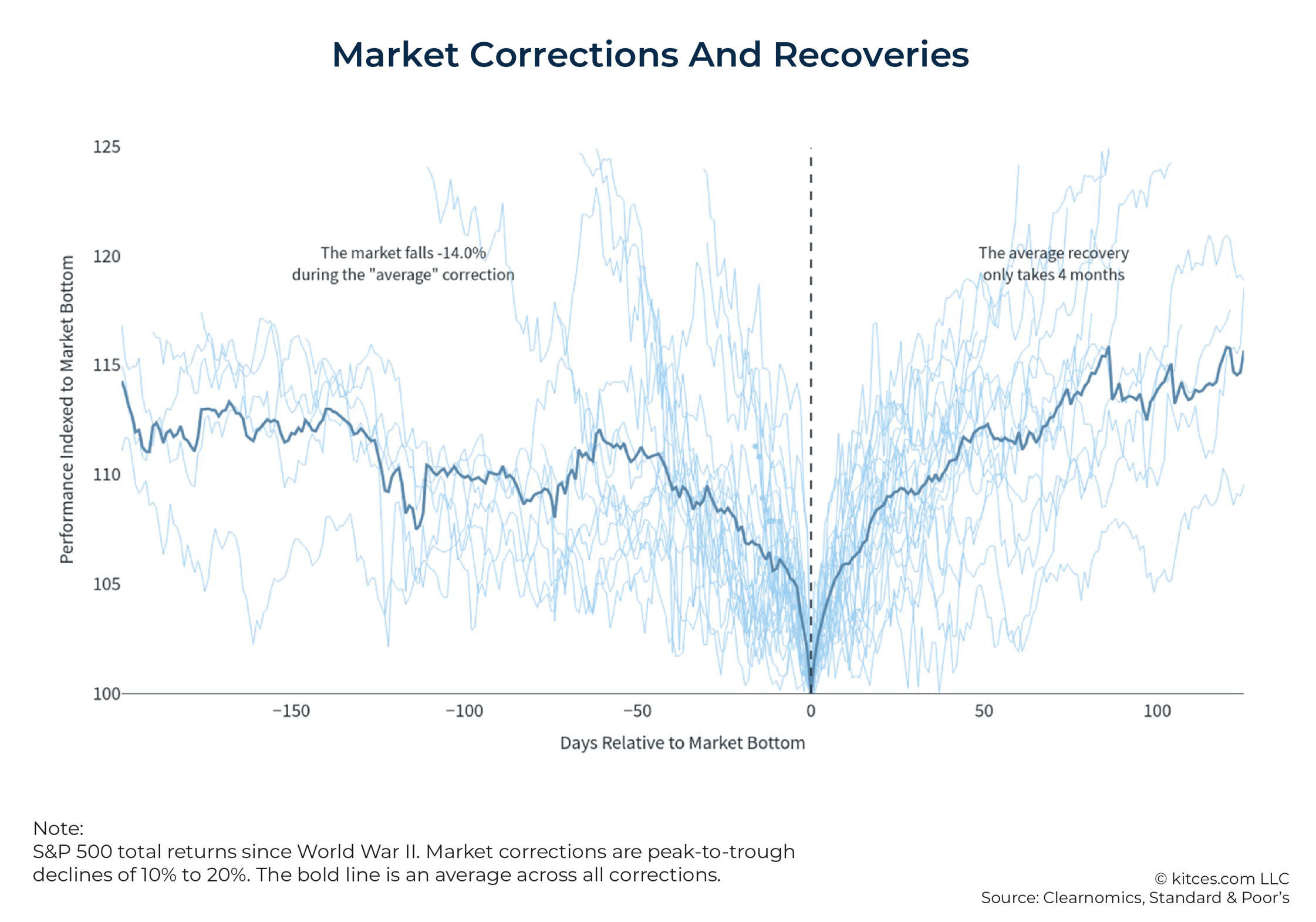

Market Corrections

Market corrections are commonly defined as declines of at least 10%. They are uncomfortable, but they are also a normal part of long-term investing. The Kitces.com graphic below illustrates historical correction averages, including the depth and approximate recovery periods of prior corrections.2

The planning lesson is not that corrections are harmless. Rather, it is that a retirement portfolio should be built with the expectation that corrections will occur. Appropriate diversification, liquidity for near-term withdrawals, and a disciplined review process can help keep short-term volatility from overwhelming the broader retirement plan.

Past performance and historical recovery periods are not guarantees of future results.

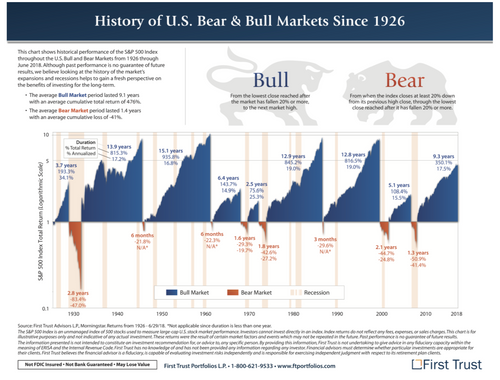

Bear Markets

Bear markets, commonly defined as declines of 20% or more, can be especially challenging for those near or in retirement. The concern is not only that account values decline. The deeper concern is that withdrawals during a decline may lock in losses and leave fewer assets available to participate in a later recovery.

The First Trust chart below provides historical perspective on bear market declines and subsequent recoveries.3 Such history can be encouraging, but retirees should still plan carefully for the possibility that recovery may take time and may not follow prior patterns.

This is where retirement investment planning differs from general investment commentary. A retiree does not need a portfolio designed only for average market conditions. A retiree needs a portfolio and income plan that can work together to support essential expenses, lifestyle goals, tax flexibility, and long-term sustainability through real-world uncertainty.

Past performance and historical recovery periods are not guarantees of future results.

The real question is not whether markets will be volatile. They will. The more helpful question is whether your retirement plan has been designed with that volatility in mind.

Our Retirement Investment Planning Approach

“Stay the course” can be good advice when the course is well designed. But in retirement, the course itself deserves careful attention. A retirement portfolio should not be viewed apart from the income plan, tax strategy, risk profile, and long-term goals it is meant to support. The portfolio’s role is to help fund the retirement paycheck, preserve flexibility, and support the broader written plan.

At KFP, our planning-first investment approach generally emphasizes five connected principles that align with our retirement income planning approach:

- Begin with the retirement paycheck the portfolio may need to support.

- Clarify dependable income sources and the income gap before designing withdrawals.

- Evaluate key retirement risks, including sequence of returns risk.

- Design a diversified, cost-conscious portfolio aligned with risk tolerance, risk capacity, time horizon, income needs, and objectives.

- Review withdrawals, cash reserves, rebalancing, taxes, and portfolio alignment as part of ongoing retirement planning support.

In short, the portfolio should serve the retirement plan—not the other way around. Investment decisions should be coordinated with income needs, tax considerations, risk capacity, personal values, and the written plan rather than treated as isolated market decisions.

Income Plan

Before focusing on portfolio design, it is helpful to understand the retirement paycheck the portfolio may need to support. Retirement income planning begins by reviewing expected spending, dependable income sources, and the income gap that may need to be filled by portfolio withdrawals, cash reserves, or other resources.

Social Security, pensions, and other more predictable income sources may cover part of a household’s essential expenses. If there is an income gap, the retirement plan can evaluate how portfolio withdrawals, cash reserves, bucket strategy, tax planning, or other planning tools may help support ongoing cash flow. The goal is not simply to generate income. The goal is to create a coordinated retirement paycheck that supports essential needs, lifestyle goals, and long-term sustainability.

When essential expenses are supported more intentionally, the investment portfolio can often be structured with clearer roles: near-term liquidity, intermediate flexibility, and long-term growth. This may help reduce pressure to sell growth assets during difficult markets and provide a clearer structure for spending decisions.

Retirement income planning describes this process as designing a coordinated retirement paycheck from the resources available to you. Investment planning should fit inside that same structure rather than stand apart from it.

For a deeper discussion of this approach, see our Retirement Income Planning webpage.

Clarify the Portfolio’s Purpose

After the retirement paycheck and income gap are understood, the next question is purpose. What is the portfolio meant to support beyond essential cash flow?

For some retirees, the portfolio may need to support regular withdrawals. For others, it may help fund travel, family priorities, charitable giving, future healthcare expenses, long-term care, or legacy goals. Some clients also want their investments to reflect personal values or faith-based considerations where appropriate.

Clarifying purpose helps turn investment planning from a general allocation exercise into a more personal retirement planning conversation. Through scenario review, planning tools can help illustrate how different choices may affect future possibilities. This is part of what KFP means by helping clients Visualize Your Retirement Possibilities™.

Purpose does not eliminate market risk, but it helps define why the portfolio exists, how much risk may be reasonable, and how investment decisions should support both the retirement paycheck and longer-term retirement goals.

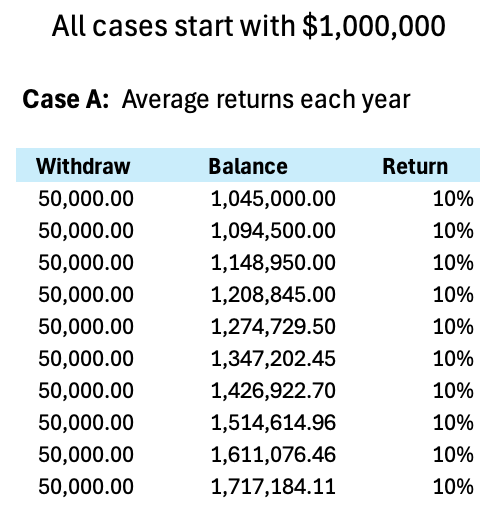

Plan for Retirement-Specific Risks

Retirement introduces risks that can be different from the risks faced during the accumulation years. One of the most important is sequence of returns risk: the risk that poor investment returns early in retirement, combined with portfolio withdrawals, may reduce the portfolio’s ability to recover over time.4

This risk is not only about the average return earned over a period of years. It is also about the order in which those returns occur. Two retirees could experience similar long-term average returns, but if one experiences negative returns early in retirement while taking withdrawals, the outcome may be very different.

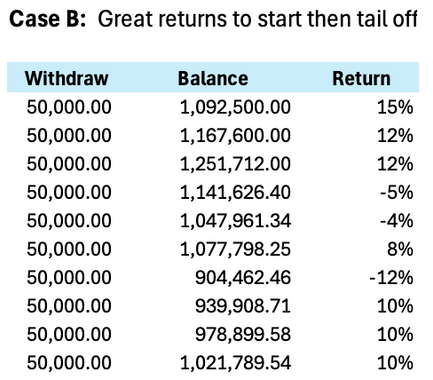

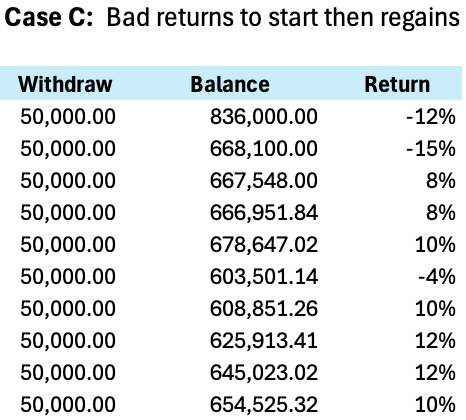

The illustrations below compare three hypothetical return patterns over a 10-year period. In each case, the starting portfolio value is $1,000,000, and annual withdrawals of $50,000 are taken. The returns are for illustrative purposes only and are not intended to represent any specific investment or market outcome.

- Case A assumes a steady 10% return each year.

- Case B assumes stronger returns occur earlier in retirement.

- Case C assumes weaker or negative returns occur earlier in retirement.

The difference between the outcomes helps show why the timing of returns can matter so much once withdrawals begin. When strong returns occur early, the portfolio has more opportunity to grow before withdrawals have a lasting effect. When negative returns occur early, withdrawals may come from a reduced portfolio balance, leaving fewer assets available to participate in a later recovery.

This is why sequence of returns risk deserves special attention for people who are within a few years of retirement or already taking withdrawals. The goal is not to predict which return pattern will occur. The goal is to design a retirement income and investment strategy that can respond thoughtfully if difficult markets arrive early in retirement.

A coordinated plan may include dependable income sources, cash reserves, a bucket strategy, diversified portfolio design, tax-aware withdrawal planning, and periodic review. No strategy can remove market risk entirely, but thoughtful planning can help reduce the likelihood that short-term volatility forces long-term decisions under pressure.

Illustrations: Sequence-of-returns examples

Case B front-loads positive returns in the early years.

Source: Kastler Financial Planning | 2025 | All rights reserved

My investment philosophy for the last 10 years has been to develop highly diversified and properly correlated portfolios, all at the lowest expense ratios possible.

Portfolio Design Considerations

KFP’s portfolio design philosophy emphasizes diversification, cost awareness, long-term discipline, and alignment with the retirement plan. Portfolio design for retirement should be built around more than a generic model or a single market index. It should reflect risk tolerance, risk capacity, time horizon, withdrawal needs, tax considerations, retirement cash flow needs, and the work the portfolio is expected to do.

Diversification may include exposure across multiple asset classes rather than relying only on large U.S. stocks or a simple stock-and-bond mix. Depending on the client’s situation, implementation may include low-cost ETFs, mutual funds, index funds, select dividend-oriented investments, and other appropriate vehicles. The objective is not to chase every opportunity. It is to create a disciplined portfolio structure that supports retirement cash flow, risk management, flexibility, and long-term goals.

For some clients, this may be expressed through a Core and Satellite structure. The Core serves as the diversified foundation of the portfolio, while Satellite allocations may be used selectively where they support income needs, values, preferences, or specific long-term objectives. Any Satellite allocation should be evaluated carefully within the broader retirement plan, risk profile, and income strategy.

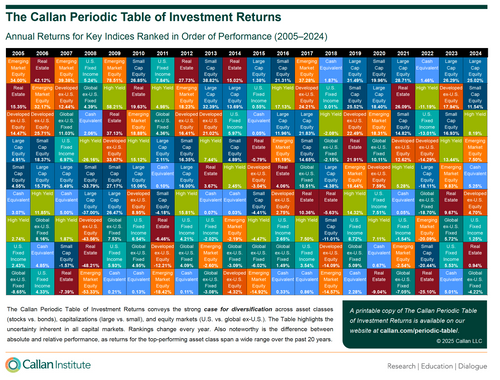

Why Diversification Still Matters

The Callan Periodic Table below illustrates how leadership among asset classes can change from year to year.5 This visual reinforces an important planning point: it is difficult to know in advance which asset class will lead or lag in any given year.

Chart: Callan Periodic Table

Bucket Strategy

A bucket strategy can be a helpful way to connect portfolio design with retirement income planning needs.6 In simple terms, assets are organized by time horizon and purpose. Instead of viewing the portfolio as one undifferentiated account balance, each part of the portfolio has a clearer job within the retirement paycheck strategy.

For example, a near-term bucket may hold cash or cash equivalents intended to support planned withdrawals over the next several years. An intermediate bucket may include more conservative or income-oriented investments designed to provide stability and flexibility. A longer-term bucket may remain invested for growth, helping support future spending needs, healthcare costs, long-term care considerations, legacy goals, or other longer-range objectives.

The purpose is not to avoid market risk entirely. Rather, the goal is to reduce the need to sell long-term growth assets during a market decline. When near-term spending needs are set aside in advance, retirees may have more flexibility to allow longer-term investments time to recover after difficult markets.

A bucket strategy can also make the retirement paycheck easier to understand. The cash reserve helps support near-term withdrawals. The intermediate portion can help bridge the gap between immediate income needs and longer-term growth. The long-term portion can remain focused on sustaining purchasing power and supporting future goals.

That said, a bucket strategy should still be managed thoughtfully. The plan needs to address how withdrawals are taken, when cash reserves are replenished, how taxes are considered, and how the portfolio is rebalanced. Without a process for maintaining the buckets, the strategy can become harder to manage over time.At KFP, bucket strategy is not treated as a stand-alone formula. It is one possible tool within a broader retirement income and investment plan. For some clients, a simplified version may work best: maintaining a near-term cash reserve while investing the remaining portfolio according to risk tolerance, risk capacity, diversification, income needs, and long-term objectives. The right structure depends on the household’s retirement paycheck, dependable income sources, income gap, tax situation, and overall plan.sign.

Portfolio Management

Portfolio management in retirement is not the same as market timing. It is not about frequent trading or trying to predict the next market move. Rather, it is about reviewing whether the portfolio remains aligned with the retirement plan, the Investment Policy Statement, the client’s risk profile, and the retirement paycheck strategy it is meant to support.

That may include periodic rebalancing, reviewing risk tolerance, evaluating cash reserves, revisiting withdrawal needs, and considering how tax planning may affect account-level decisions. Life changes, market changes, and planning assumptions can all affect whether adjustments are needed.

In that sense, portfolio management is part of ongoing retirement planning support. The goal is not to react emotionally to every market movement. The goal is to steward the portfolio with discipline so it continues to serve the broader retirement plan.

Questions to Consider About Your Retirement Portfolio

- Do I have a clear process for reviewing and rebalancing the portfolio over time?

- Is my portfolio designed around my retirement paycheck, or only around investment growth?

- Do I know where withdrawals would come from during a market decline?

- Have I considered how taxes may affect my retirement income strategy?

- Does my portfolio still reflect my current risk tolerance and risk capacity?

How KFP Can Help Bring the Pieces Together

At Kastler Financial Planning, investment planning is part of a broader retirement planning services. Through the 7 Pillars Retirement Planning® framework, we evaluate portfolio design alongside retirement income planning, tax planning, risk analysis, healthcare considerations, long-term care planning, and estate and legacy goals.

For retirees and those approaching retirement, this means the portfolio is not reviewed in isolation. We consider how it fits with your retirement paycheck, dependable income sources, income gap, withdrawal needs, tax picture, risk tolerance, risk capacity, and long-term goals.

That process may include reviewing whether your portfolio is appropriately diversified, whether cash reserves or a bucket strategy may be appropriate, how withdrawals may be handled during difficult markets, and whether the portfolio still reflects the level of risk you are both willing and able to take.

For clients who want continued support, investment management can also be coordinated with ongoing retirement plan monitoring and periodic reviews. The goal is to help keep the portfolio aligned with the broader retirement plan as markets, tax laws, income needs, and life circumstances change.

No planning process can remove market uncertainty or guarantee future outcomes. But thoughtful retirement investment planning can help bring structure, clarity, and discipline to decisions that may otherwise feel reactive during unsettled markets.

A Thoughtful Next Step

If recent market volatility has left you wondering whether your portfolio is still aligned with your retirement income needs, it may be a good time to review the plan before making major changes.

We invite you to begin with a no-charge, no-obligation consultation — a thoughtful first conversation about your retirement paycheck, your investment questions, and the broader plan your portfolio is meant to support.

We Help You Visualize Your Retirement Possibilities™

Citations

1. Time in the Market vs. Timing the Market chart, source URL on file: https://1818132.hs-sites.com/hs/home

2. Kitces.com, market correction graphic, source URL on file: https://www.kitces.com

3. First Trust Portfolios, bear market declines and recoveries chart, source URL on file: https://www.ftportfolios.com/Index.aspx

4. Kiplinger, “Sequence-of-Return Risk: How Retirees Can Protect Themselves,” https://www.kiplinger.com/retirement/sequence-of-return-risk-how-retirees-can-protect-themselves

5. Callan, “2024 Classic Periodic Table,” https://www.callan.com/research/2024-classic-periodic-table/

6. Investopedia, “Comparison: Bucket Strategy vs. Systematic Withdrawals,” https://www.investopedia.com/articles/financial-advisors/060815/comparison-bucket-strategy-vs-systematic-withdrawals.asp

{kind=link}

{kind=link}