“How Much Are Advisory Fees Costing You? Let’s Find Out.”

Every dollar you invest should work for you—not for someone else’s fee structure.

As a fiduciary financial advisor, I charge low-cost flat fees. I often hear from investors who assume they’re getting a fair deal because their advisor charges the “standard” 1% assets under management (AUM) fee. But when you zoom out over time and apply some analytical rigor, that seemingly small 1% becomes a massive drag on long-term growth—especially when compounded over your retirement time horizon.

To illustrate the difference, I built a comprehensive fee analysis spreadsheet that compares my low flat fees to the industry-standard AUM model. It’s not just a sales pitch—it’s a reality check. You can download it and run your own numbers to see how much you might be leaving on the table. The results are eye-opening.

💰 The Hidden Cost of “Standard” Fees

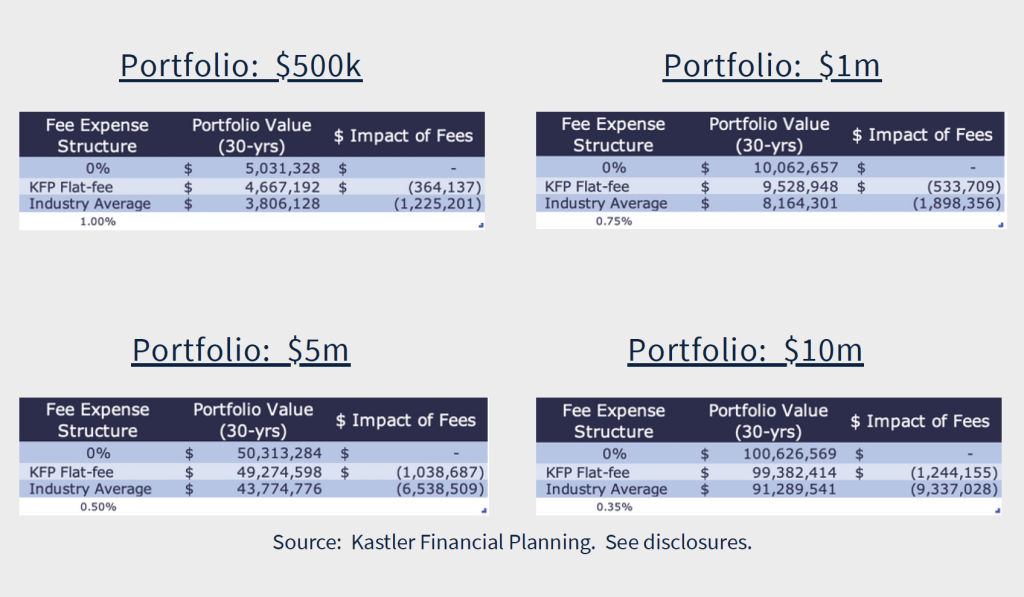

Let’s say you have a $1 million portfolio growing at a solid 8% annual rate over 30 years. Under the typical 1.25% AUM structure, you’re paying fees on the entire growing portfolio, not just on your gains. That compounds into serious money. Comparing no fees to a 1.25% fee to no fee or our flat fee:

• No fees, 8% growth for 30 years → Your portfolio grows to $10 million

• 1.25% AUM fee, 8% growth for 30 years → Your portfolio tops out at $7 million

• Our flat fee tier structure, 8% growth for 30 years → Your portfolio tops out at $9.5 million

You read that right—more than one-third of your ending value gone, just due to the “standard” fee.

Here are 4 example portfolios comparing the portfolio value lost due to AUM fees. Each example is calculated with straight line 8% growth for 30 years and 3 fee scenarios: no fee, average %AUM, and our flat-fee structure.

🧠 Flat-Fee Planning: Transparent, Scalable, Ethical

We charge a straightforward, transparent annual fee that reflects the planning work performed—not the size of your portfolio. Benefits over competition:

• You know exactly what you’re paying every year

• You’re not penalized for growing your wealth within a given tier

• You get fiduciary-level planning without sales pressure or hidden incentives

And most importantly, your investment growth stays where it belongs: in your account.

The spreadsheet we offer allows you to compare your current fees with a flat-fee model across different portfolio sizes, and growth scenarios over a 30-year period. You can tweak variables to see your real cost—and your potential savings.

📊 Why This Matters More Than Ever

In today’s volatile markets and shifting regulatory landscape, clarity is priceless. The One Big Beautiful Bill Act (OBBBA) has already started reshaping tax and retirement rules and keeping your investment strategy lean and nimble is no longer optional—it’s essential.

Clients who pay less in fees have a greater buffer for risk, flexibility in retirement planning, and more room to adapt as laws evolve. If you’re working with a traditional AUM advisor, take a moment to ask: What are you really getting for that 1%?

If it’s asset allocation and quarterly check-ins, it might be time to reevaluate.

🔍 Seeing Is Believing

That’s why I created this spreadsheet—not just to talk about the value of flat fees, but to show it. If you’re a DIY-minded investor, or simply someone who wants more clarity around the true cost of advice, this tool will empower you to compare.

You’ll be able to:

• Input your current portfolio and AUM fee

• Set your expected return

• See total fees paid, ending portfolio values, and how flat fees stack up

• Visualize your opportunity cost over time

You’ll quickly discover that my approach isn’t just competitively priced—it’s structurally built to favor your long-term success.

🚀 The Fiduciary Difference

My practice is built on fiduciary ethics and low-cost planning because I believe financial advice should help you build wealth, not quietly siphon it away. The spreadsheet is one way I prove that principle.

Whether you’re just starting your retirement planning journey or reevaluating your current advisor, it’s worth seeing the numbers side by side. If you’re paying 1% or more, and you’re not getting comprehensive, strategic advice tailored to your life—why not get the clarity you deserve?

📥 Ready to Compare?

Download the no-cost, no-obligation spreadsheet from Kastler Financial Planning and see for yourself how flat fees could mean millions more in your pocket. It’s your money. Let’s keep it working for you.

👉 Download Fee Comparison Spreadsheet Here:

Resources – Kastler Financial Planning

How We Can Help

Our goal is to help you achieve your Purposeful RetirementTM. Income Planning, Tax Planning, and Investment Planning are the 3 key pillars to our 7 Pillars Retirement Planning® approach. Health, Long-Term Care, Risk Analysis, and Estate Planning round out the 7 pillars we can help you with to prepare your personalized retirement plan.

Mike Kastler has been performing financial planning and retirement planning since 2015. He has a Master of Science in Finance and the prestigious designation Retirement Income Certified Professional®. As a Fee-Only, Fiduciary, and Independent professional it is a client-first/planning-first approach. No commissionable products are sold and Assets Under Management (AUM) services are provided as a flat-fee service, not a % of AUM. More About Us here: KastlerFinancialPlanning.com/about

We Help You Visualize Your Retirement Possibilities

{kind=link}

{kind=link}